Real Estate

First-Time Home Buyers A Complete Guide to the Home Buying Journey

April 18, 2026

Navigate the home buying journey with confidence! Learn essential tips, financing options, and common pitfalls to ensure successful homeownership.

Embarking on the journey to homeownership is both exciting and challenging, especially for first-time home buyers navigating today’s competitive real estate market.

Recent trends show that while many millennials aspire to own a home, rising property prices, strict mortgage requirements, and competitive bidding wars often make the process difficult to navigate.

Understanding the home buying process is essential for making informed decisions, securing financing, and avoiding costly mistakes. From getting pre-approved for a mortgage to analyzing market conditions and closing the deal, each step plays a critical role in successful homeownership.

This guide provides a clear, step-by-step overview of the home buying journey, helping first-time buyers understand what to expect and how to confidently move toward owning their first home.

What Do We Mean by "1st Time Home Buyers" and Why is This Important?

A first-time home buyer (FTHB) is typically defined as someone who has not owned a home within the last three years. This classification is crucial because it opens the door to various benefits tailored specifically for this demographic in the real estate market. FTHBs represent a potent segment of homebuyers, often constituting a significant portion of real estate transactions. Recent trends reveal a burgeoning influx of millennials and younger generations entering the market, driven by economic factors paired with aspirational desires for home ownership.

The significance of FTHBs cannot be overstated; they invigorate the housing market and contribute to a more vibrant economy. Numerous state and local governments have established programs designed to aid FTHBs. These include favorable options such as lower down payment requirements—often ranging from 3% to 5%—and grants that can cover closing costs. For instance, the Federal Housing Administration (FHA) offers loans that accommodate lower credit scores and down payments, thereby enhancing accessibility to homeownership. Being well-versed in FTHB status aids buyers in navigating their options while also assisting lenders and policymakers in effectively addressing their needs. As the housing market continuously evolves, an understanding of who fits the first-time buyer profile is essential for making judicious decisions throughout the buying journey.

Financial Readiness: The Key Step Before House Hunting Begins

Prior to delving into the exhilarating pursuit of house hunting, it is vital to establish a robust financial foundation. First, set a realistic budget by assessing how much you can afford without placing undue strain on your finances. This involves evaluating your income, monthly expenses, and savings. A critical step in this process is understanding your credit score, as it plays a significant role in determining your mortgage options. A higher score typically translates to lower interest rates, thus resulting in substantial savings over time.

Next, familiarize yourself with down payment requirements, as they vary significantly based on loan types. In general, conventional loans may necessitate down payments of 5-20% of the home’s purchase price, while FHA loans might require only 3.5%. Awareness of these percentages informs your savings goals and helps in setting your prospective budget accordingly.

To help manage your finances efficiently, consider using budgeting tools such as Mint or YNAB (You Need A Budget). These resources aid in tracking your spending and ensuring you stay on target with your savings plans. Additionally, creating a dedicated savings account for your down payment offers a motivational boost to save consistently.

In summary, aspire for a comprehensive approach to financial readiness that combines a clear understanding of your finances, an effective saving strategy, and an awareness of potential mortgage options. By adequately preparing your finances, you will not only enhance your confidence but also alleviate some of the stress characteristic of purchasing your first home.

Decoding Mortgages and Exploring Loan Options

For first-time home buyers, maneuvering through the mortgage landscape can be intimidating. Familiarity with the types of loans available is crucial for making smart decisions. Common options include fixed-rate mortgages, characterized by consistent interest rates maintaining throughout the loan duration, offering predictable monthly payments. In contrast, adjustable-rate mortgages (ARMs) come with rates that can fluctuate over time, initially offering lower rates than fixed-rate loans but introducing potential uncertainty regarding future payments.

Another frequently utilized option is the FHA loan, which holds particular appeal for FTHBs due to its lower down payment requirements and more lenient credit score criteria. However, it’s vital for buyers to be cognizant of mortgage insurance, which is often necessary for lower down payments. This insurance acts as a safeguard for lenders in the event of borrower default, hence incurring an additional monthly cost that could influence the overall affordability of the mortgage.

Interest rates and points also significantly impact the overall cost of a loan. Points refer to fees paid upfront to reduce the interest rate, altering long-term expenses. Therefore, buyers should meticulously weigh these financial variables against their individual financial situations.

To adeptly navigate these mortgage options, FTHBs are strongly encouraged to consult with mortgage professionals. These experts can provide customized advice, clarify complex terminology, and assist buyers in identifying the best loan options tailored to their unique needs and financial aspirations.

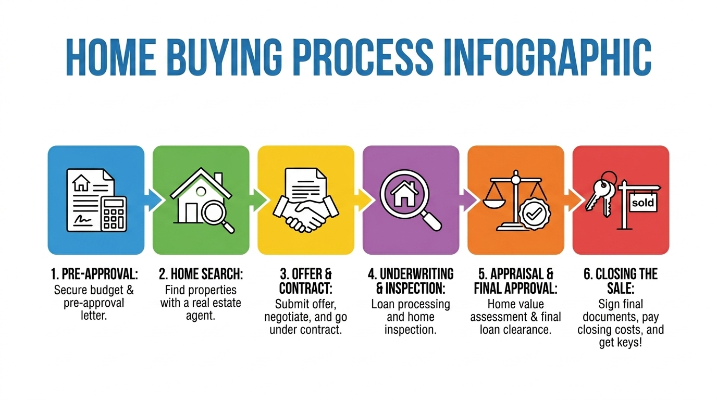

The Home Buying Process: A Step-by-Step Guide

1) Mortgage Pre-Approval

Before embarking on house hunting, securing pre-approval for a mortgage is imperative. This process typically spans from a few days to a week and involves submitting a loan application alongside financial documentation to a lender. Gaining pre-approval not only clarifies your budget but also demonstrates to sellers that you are a serious buyer. Potential challenges during this process can arise from inconsistencies in your credit report and the assessment of your debt-to-income ratio, both of which could influence loan approval.

2) Collaborating with a Realtor to Find Your Home

Once the financing is secured, the next step involves searching for homes. Collaborate with a reputable realtor who comprehends your preferences and local market trends. This phase can last from several weeks to several months, depending on your criteria. Be prepared to face challenges such as heightened market competition and limited inventory, potentially prolonging your search.

3) Formulating an Offer and Engaging in Negotiations

Upon discovering a home you adore, the subsequent action is to formulate an offer. Partner with your realtor to ascertain a fair price based on comparable property sales in the vicinity. Negotiations can unfold over a few days, with possible counteroffers exchanged. Key considerations here include grasping local market conditions while remaining flexible with a backup plan should your offer not be accepted.

4) Home Inspections and Property Appraisal

Once your offer is accepted, arrange for a home inspection and appraisal to evaluate the property’s condition and market value. Inspections usually last several hours, with reports available in a few days. Being prepared for potential inspection issues—such as necessary repairs—can mitigate delays in the buying process.

5) Successfully Closing the Sale

The final stretch involves the closing phase, where you sign documents and formally transfer ownership. This process can extend over several hours and usually occurs 30-45 days post-acceptance of your offer. Stay vigilant for common hurdles like last-minute financing changes or appraisal disputes that can hinder closing. Being adequately prepared, which includes having all necessary documents ready, will pave the way for an uneventful completion of your home purchasing adventure.

Navigating Common Pitfalls Faced by First-Time Buyers

Venturing through the home buying process for the first time can be overwhelming, and many first-time buyers often find themselves falling into common pitfalls. One major blunder involves underestimating the total costs associated with homeownership. Beyond the mortgage payment, new homeowners should budget for ongoing expenses such as maintenance, property taxes, insurance, and utilities. For instance, while a buyer might secure a home for $300,000, failing to account for an additional $5,000 annually in maintenance and taxes could lead to financial strain.

Another prevalent oversight is heavily relying on online property value estimates. Although platforms like Zillow provide quick price approximations, they frequently overlook the nuances that a professional appraisal or local market expertise offers. Seeking professional guidance is essential for acquiring a nuanced understanding of a property's true value.

Lastly, overlooking the necessity of home inspections can result in expensive surprises in the future. Buyers enamored with a home’s aesthetic appeal may miss underlying issues such as plumbing faults or roof leaks without a thorough inspection. Dedicating time to due diligence—like hiring a qualified inspector—can save buyers from unexpected financial burdens. By recognizing these pitfalls and soliciting guidance, first-time homebuyers can make informed decisions and embark on a pathway towards successful homeownership.

Life After Buying Your First Home

After the acquisition of your first home, several pivotal considerations emerge. Firstly, ensuring adequate home insurance is crucial for safeguarding your investment against unforeseen circumstances. Next, assess any immediate enhancements or repairs required upon moving in to guarantee your living space is both comfortable and functional. Moreover, maintaining an ongoing budget for expenses—such as property taxes, utility bills, and routine maintenance—is essential for effective financial management. Remember, homeownership not only provides stability but also serves as a stepping stone towards improved personal finance. Embrace this journey with a proactive mindset, continually seeking ways to invest in and maintain your new home.

A Bright Path Forward

In the realm of homeownership, making informed purchasing decisions is paramount for achieving a fulfilling and successful experience. Throughout this guide, we have underscored vital components of the home buying journey—ranging from financial preparation to embracing mortgage decisions and avoiding common pitfalls. For first-time buyers, harnessing this knowledge not only empowers you but also lays down a solid foundation for a prosperous future. As you take strides towards homeownership, consider this guide as your trusted companion, inspiring you to make choices that resonate with your aspirations and long-term goals.

Homeownership can indeed be a dream within reach—leverage the insights you’ve gained to compose a thriving and satisfying future.

Just For You

Parenting

Is Diarrhea Normal During Pregnancy Causes and When to Worry

May 23, 2026

Pets

Cat Feeder Guide Types, Features, and How to Choose the Right Feeding Solution

April 7, 2026

Tourism

Best Travel Destinations Japan A Practical Guide to Exploring Cities, Nature, and Culture

March 27, 2026

Shopping

Personalized Gifts for Grandma That Feel Thoughtful and Truly Meaningful

April 13, 2026

Recommended For You

Parenting

What Are the Pregnancy Symptoms A Clear Guide to Early Signs and Timing

April 14, 2026

Pets

How to Train a Cat With Positive Reinforcement

June 6, 2026

Tourism

Best Places to Travel Solo Safe and Inspiring Destinations

April 27, 2026

Shopping

Meaningful Choices The Ultimate Guide to Personalized Baby Gifts

April 21, 2026