Real Estate

Mortgage Interest Rates Explained Simply What You Should Know

April 24, 2026

Navigate the complexities of mortgage interest rates for first-time home buyers. Discover tips, programs, and factors affecting your mortgage rates.

Buying a home for the first time can feel like a challenging endeavor, particularly when it comes to grappling with mortgage interest rates—a critical factor affecting overall housing costs. Addressing the question, Do first-time home buyers get better interest rates? is essential for informed financial planning. This inquiry holds substantial implications, as comprehending mortgage pricing intricacies can lead to significant savings or unnecessary costs over the lifetime of a loan. In this article, we will examine the elements that impact mortgage rates, dispel prevalent myths, and arm first-time buyers with the essential knowledge needed to make sound decisions. By enhancing your understanding of interest rates, you will be better prepared to navigate the home buying process with confidence.

How Mortgage Interest Rates Actually Work in Real Life

Mortgage interest rates lack a universal standard; they can fluctuate significantly based on numerous factors. Lenders predominantly establish these rates according to prevailing market conditions and the individual profiles of borrowers. Economic indicators such as employment rates, inflation, and the overall GDP growth are crucial in shaping market trends. During periods of economic prosperity, demand for loans often drives rates higher, while economic slowdowns can lead to lowered rates as a means to encourage borrowing and spending.

Lenders also evaluate each borrower’s credit profile and financial status, analyzing credit scores, income stability, and debt-to-income ratios. Borrowers who present as low risk—often characterized by high credit scores—typically qualify for more favorable rates. On the other hand, individuals deemed higher risk may face elevated rates. Additionally, policy decisions made by federal institutions, including the Federal Reserve, further influence mortgage rates as they affect the larger economy's monetary supply and cost of funds. For first-time buyers, being aware of these variables is crucial in navigating the mortgage landscape, as they directly impact the affordability of purchasing a home.

Do First-Time Home Buyers Actually Get Better Interest Rates?

The notion that first-time home buyers automatically receive better interest rates compared to their seasoned counterparts is a common misinterpretation of the market. While certain assumptions suggest that new buyers might benefit from preferential rates due to their status, the truth is more complicated. Various elements such as credit scores, down payment amounts, and general financial health chiefly determine mortgage interest rates.

Lending policies can impact rates, especially for targeted first-time buyer programs. Initiatives such as those facilitated by the Federal Housing Administration (FHA) or specific local assistance programs offer favorable loan terms, which could potentially lead to lower interest rates. These programs frequently require smaller down payments and can assist those with less-than-ideal credit scores, creating opportunities for first-time buyers to access competitive rates.

Nevertheless, seasoned buyers often possess advantages of their own, such as established credit histories and the financial capability to make larger down payments, which can translate into lower rates. As such, while first-time buyers might have access to specialized programs, it is crucial for them to assess their unique financial situations and consider all available options, as better rates are not guaranteed.

Programs That May Help First-Time Buyers Lower Their Rate

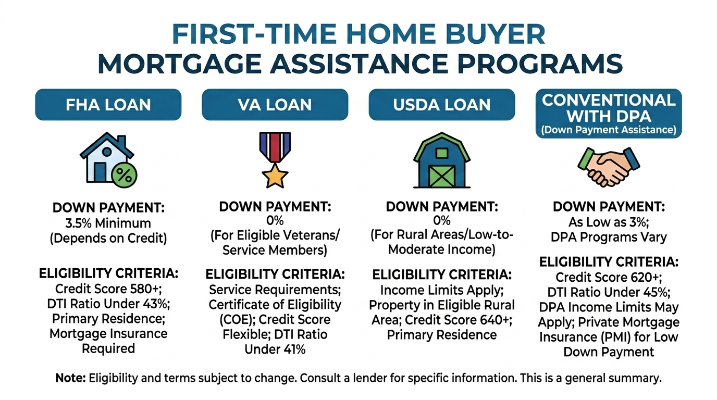

First-time home buyers have a diverse range of mortgage programs available that can reduce their financial strain and potentially lower their interest rates. Notably, government-backed loans, including Federal Housing Administration (FHA) and Veterans Affairs (VA) loans, cater specifically to new buyers.

FHA loans are particularly beneficial as they allow buyers with lower credit scores to access homeownership with minimal down payments—sometimes as low as 3.5%. This inclusivity helps to make the dream of owning a home attainable for many. In contrast, VA loans serve veterans and active duty military personnel, often providing attractive terms like no down payment and lower interest rates compared to conventional financing.

Moreover, numerous state and local governments have implemented financial assistance programs aimed at further lowering rates for first-time buyers. These initiatives can include grants or forgivable loans designed to cover down payments and closing expenses, substantially decreasing the initial cost burden. For example, state housing finance agencies frequently introduce programs specifically intended for first-time buyers, helping them secure favorable terms and rates. Through thorough exploration of both federal and local resources, first-time buyers can identify a mortgage solution that aligns with their financial goals and aspirations.

What Really Impacts the Interest Rate You Receive

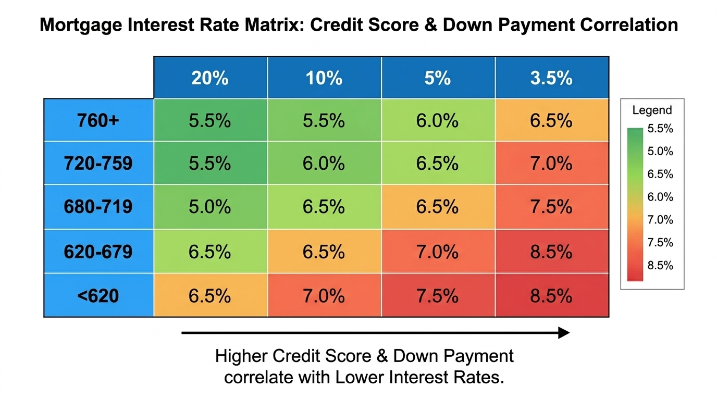

Securing a mortgage involves various pivotal factors that heavily dictate the interest rate you may be offered. Chief among these is your credit score, which serves as a significant risk indicator for lenders. Higher credit scores—typically above 740—are often rewarded with lower rates, while a borrower with a score as low as 620 can expect to face rates well above 4.0%, whereas someone at 720 might see rates as low as 3.5%.

Another crucial element impacting mortgage rates is the down payment. Generally, a larger down payment can reduce the lender's perceived risk and lead to more attractive rates. For example, a buyer making a 20% down payment could qualify for a significantly better rate than someone who meets only the minimum 5%.

Furthermore, the type of loan under consideration is essential, as rates can differ considerably between conventional, FHA, and VA loans, with government-backed loans often resulting in lower costs due to their respective insurance and guarantees. Lastly, your debt-to-income (DTI) ratio, which measures total monthly debt against gross monthly income, is a key factor; lenders generally prefer applicants with lower ratios since they indicate a healthier financial situation. An individual with a DTI of 36% is typically viewed more favorably than one who has a DTI of 45%. Gaining insight into these aspects can empower first-time buyers to navigate the mortgage market more effectively.

Why Two Buyers Can Get Completely Different Rates

When two prospective buyers with seemingly similar financial backgrounds approach lenders for a mortgage, they might find themselves facing starkly different interest rates. This divergence can primarily be attributed to the discretion exercised by lending institutions, which evaluate borrowers on an individual basis, assessing their risk before setting rates. For instance, one buyer may have a marginally higher credit score or demonstrate better debt management, which could yield a more appealing rate, whereas the other might fall into a higher-risk category.

Moreover, competition among lenders also plays a substantial role. In a robust and competitive lending environment, institutions may offer lower rates to attract clients, which can further complicate rate comparisons.

Timing and external variables can dramatically shift the interest rate landscape. Economic fluctuations, regulatory changes, or shifts in the Federal Reserve's interest rates can all impact borrowers differently. Additionally, geography can lend itself to rate discrepancies, with buyers in highly sought-after markets often facing elevated rates compared to those securing loans in less competitive regions.

Enhancing Your Chances for a Lower Rate

For first-time home buyers, elevating the chance for a lower mortgage rate can profoundly affect the overall cost of homeownership. Here are crucial steps to improve your odds:

- Enhance Your Credit Score: Work towards improving your credit score, as there is a direct correlation between higher scores and reduced interest rates. Make punctual payments on outstanding debts and strive to minimize credit utilization.

- Aim for a Larger Down Payment: A substantial down payment helps decrease your loan-to-value ratio, frequently leading to more favorable rates. Target a down payment of at least 20% if feasible, which also can help you circumvent private mortgage insurance (PMI).

- Shop Around for Lenders: Do not settle for the first mortgage provider you approach. Investigate and compare multiple lenders to uncover the most competitive rates, as there can be significant discrepancies between offerings.

- Consult Mortgage Advisors: Engage with mortgage advisors who can skillfully navigate the complexities of the market and assist in identifying solutions tailored to your financial landscape.

By adhering to these guidelines, first-time buyers will find themselves in a more advantageous position when applying for a mortgage, translating to substantial savings over time.

Setting the Stage for Homeownership

In summary, grasping the intricacies of mortgage rates is vital for first-time home buyers amidst a convoluted housing market. This article illustrated that while being a first-time buyer doesn't inherently guarantee better rates, several influential elements—like credit scores, down payments, and economic conditions—play critical roles in determining mortgage pricing. Additionally, exploring advantageous programs can increase the likelihood of securing better terms. As potential homeowners, seeking personalized financial guidance will help tailor decisions to unique circumstances, paving the way to informed actions. With knowledge and appropriate support, first-time buyers can boldly embark on their journeys to homeownership, transforming their aspirations into reality.

Just For You

Parenting

The Significance of Sleep Training for Parents and Babies

April 28, 2026

Pets

The Allure of Long-Furred Cat Breeds

May 19, 2026

Tourism

Best Hidden Gems in the United States 2026 Travel Guide

April 29, 2026

Shopping

The Best Adidas Running Shoes Finding the Perfect Balance for Every Runner

April 11, 2026

Recommended For You

Parenting

Circumcision Care for Newborns A Practical Guide for Parents

April 25, 2026

Pets

How to Train Your Cat to Use Kitty Litter A Simple Guide for New Cat Owners

April 10, 2026

Tourism

Best Hidden Gems in the United States 2026 Travel Guide

April 29, 2026

Shopping

Unlocking Value The Best Cheap Running Shoes That Don’t Skimp on Comfort

April 13, 2026