Real Estate

How Much House Can I Afford With 80K Salary A Realistic Breakdown for Homebuyers

April 4, 2026

Thinking of buying a home with an $80K salary? Discover how much house you can afford with our detailed breakdown of finances, budgeting, and market factors.

Home affordability is not merely a financial indicator; it plays a pivotal role in the home-buying journey, particularly for individuals facing one of life's most significant financial commitments. For prospective buyers with an $80,000 annual salary, understanding how much house they can afford becomes imperative to avoid costly pitfalls. Various factors—such as existing debt, credit scores, and fluctuating interest rates—significantly influence purchasing power. Comprehending these elements can empower prospective homeowners, facilitating informed decision-making that yields long-lasting benefits. In this article, we delve into the intricate relationship between income and home affordability, providing clarity on the path to homeownership.

How Income Really Translates Into Home Buying Power

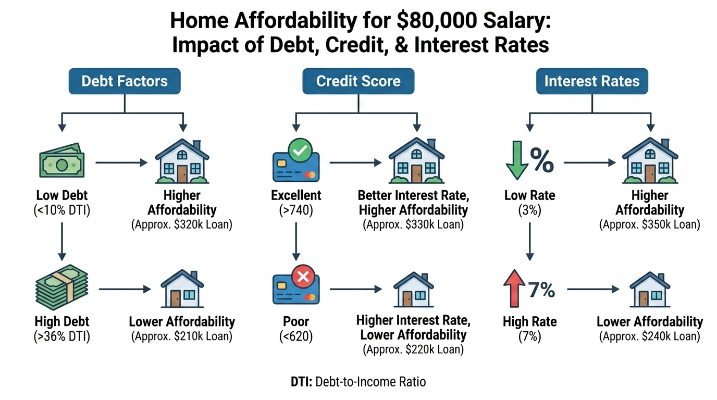

Lenders prioritize evaluating a prospective homebuyer's ability to afford a property by focusing primarily on income and its stability. They assess several financial components, including base salary, additional income streams, and employment history. In the case of an individual earning $80,000, lenders typically use the debt-to-income (DTI) ratio as a crucial metric—usually, this ratio should not surpass 43%. Essentially, for someone with an annual income of $80,000, comfortable monthly mortgage payments hover around $2,500, contingent upon existing debt levels.

However, geographic and local market conditions substantially affect the true purchasing power of that salary. For instance, in high-cost areas like San Francisco, where median home prices soar above $1 million, an $80K salary may afford only a modest condo. Conversely, in cities like Cleveland, where homes can be listed for under $250,000, the same salary might secure a more spacious family residence. Furthermore, local fluctuations in interest rates and housing demand can shift the landscape of affordability dramatically. Statistics indicate that while an $80K salary seems adequate on a national scale, regional economic factors can significantly alter its practical application in various housing markets.

Why an $80K Salary Doesn’t Equal One Fixed House Price

For homebuyers earning $80,000, it’s essential to recognize that housing prices can vary greatly based on geographic location and local market dynamics. A $300,000 home in a thriving metropolitan area may provide only a compact two-bedroom unit, while the same budget might allow for a generous three-bedroom home in a rural community. This stark contrast underscores how urban demand inflates prices and subsequently affects affordability.

Other market conditions intensify these price differences. In a seller's market characterized by high demand relative to supply, fierce competition among buyers can incite bidding wars, driving prices beyond reasonable estimates. Conversely, in a buyer's market where supply exceeds demand, home prices may substantially drop, presenting unique opportunities for individuals earning an $80K salary. Moreover, the type of property significantly influences price; newly constructed single-family homes often command higher prices compared to older, multifamily residences.

Ultimately, recognizing these factors is vital for buyers with an $80,000 salary. It enables them to set realistic expectations concerning home type and location, and better equips them to navigate the unpredictable homebuying landscape.

The Role of Debt-to-Income Ratio in Mortgage Approval

The debt-to-income (DTI) ratio is a critical measure that lenders use to ascertain a borrower's ability to manage monthly payments and meet debt obligations. This ratio is calculated by dividing total monthly debt payments by gross monthly income, presenting it as a percentage. A lower DTI is preferable, as it suggests to lenders that the borrower is less likely to default on loans. Most lenders generally favor a DTI of 36% or lower for mortgage approval, although some may allow a slightly higher ratio under specific conditions.

For an individual with an annual income of $80,000, this equates to approximately $6,667 in gross monthly earnings. Establishing a DTI of 36% would permit total monthly debt payments of around $2,400. This figure encompasses all debts—such as mortgages, car loans, and credit card payments. For example, if a borrower incurs $400 from car payments and $200 for credit cards, they would need to maintain their mortgage payment at around $1,800 to keep a healthy DTI. Understanding and managing the DTI ratio is crucial for prospective homebuyers, as it heavily influences both borrowing potential and mortgage conditions.

What Monthly Mortgage Payment an $80K Income Can Support

For those earning an annual income of $80,000, grasping the components of a mortgage payment is pivotal in assessing home affordability. The general guideline suggests that the total monthly housing expense, which includes principal, interest, taxes, and insurance (often referred to as PITI), should ideally not exceed 28% of one's gross monthly income. For an individual making $80K, this monthly limit translates to about $1,867.

To compute monthly mortgage payments, you can apply the following formula:

M = P[r(1 + r)^n] / [(1 + r)^n – 1]

Where:

- M = total monthly mortgage payment

- P = principal loan amount

- r = monthly interest rate (annual rate / 12)

- n = number of payments (loan term in months)

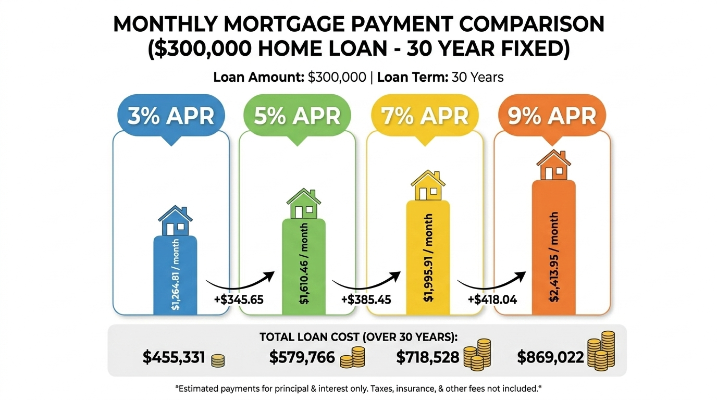

Let’s illustrate with a couple of scenarios: Suppose you consider a 30-year mortgage with a 3% interest rate on a $300,000 home loan, leading to a monthly payment of about $1,265. However, if the interest rate increases to 5%, that payment escalates to approximately $1,610. Thus, understanding how interest rates fluctuate is essential as they significantly impact monthly payments, emphasizing the need to factor in prevailing rates when calculating home affordability.

Hidden Costs That Affect Affordability More Than Expected

Homeownership encompasses far more than the mere monthly mortgage payment; numerous hidden expenses can dramatically influence overall affordability. Principal among these costs are maintenance, typically averaging roughly 1% of the property's value annually, which equates to $2,000 each year for a home valued at $200,000. Property taxes serve as another substantial expense, often ranging between 1% to 2% of the property value, which can impose upwards of $4,000 annually on homeowners. In addition, homeowners' insurance, averaging around $1,200 per year, compounds the financial obligations alongside utility bills, which can range from $300 to $400 monthly, contingent upon the home's size and location.

These supplementary costs underscore the critical importance of exhaustive budgeting for prospective homebuyers. It is vital to include these anticipated costs in one’s financial planning to avoid underestimating the actual price of homeownership. By cultivating a comprehensive understanding of monthly expenses, individuals can make well-informed decisions, ensuring that their desired home stays within reach while maintaining a healthy financial posture. A robust financial strategy is crucial for successfully navigating the intricacies of homeownership while securing a sustainable living environment.

How to Calculate Your Own Safe Home Budget

Establishing a safe home budget tailored to your specific financial situation involves several indispensable steps. Start by assessing your total monthly income, ensuring to incorporate all revenue streams, including bonuses or side jobs. Next, compute your overall monthly expenses, covering essentials such as groceries, utilities, and any debts; employing the DTI guideline (striving for under 36% is advisable) can be beneficial here.

After determining your monthly income, deduct your monthly expenses to unveil how much you can allocate toward housing costs, ideally keeping it below 28% of your income. Once you arrive at a targeted monthly payment range, factor in additional expenses like property taxes and insurance. Utilizing a spreadsheet tool or budgeting app can assist in these calculations; software options like Mint or YNAB are excellent for tracking expenses against a budget effectively.

Lastly, while these initial steps provide a framework for understanding your financial limits, consulting a mortgage advisor is highly advisable to gain personalized insights based on current market conditions. This professional guidance can open up tailored options suitable for your situation. By taking these proactive steps, you will empower yourself to navigate your home-buying journey with confidence.

Your Path to Homeownership Awaits

In essence, an $80,000 salary opens diverse avenues for homebuyers, yet understanding one's finances is paramount. Central to this journey are the key considerations of debt-to-income ratios, unexpected hidden costs, and feasible budgeting strategies. Through an elaborate evaluation of these elements, prospective buyers can make informed purchasing decisions aligned with their financial realities. Embracing this foundational knowledge ensures not only financial stability but also a fulfilling homeownership experience. Remember, the journey to finding the right home is a pursuit of balance between dreams and practicalities, allowing you to establish a cherished space while safeguarding your fiscal health.

Just For You

Parenting

Baby Formula Feeding Chart An Essential Guide for New Parents

April 24, 2026

Pets

How to Train Your Cat to Use Kitty Litter A Simple Guide for New Cat Owners

April 10, 2026

Tourism

Best Destinations to Travel in June Where the World Feels Just Right

April 17, 2026

Shopping

The Heart of Gifting Finding the Perfect Birthday Gift for Your Mom

April 18, 2026

Recommended For You

Parenting

Can Babies Sleep on Their Stomach Safety Rules and Age Guidelines

May 18, 2026

Pets

How to Train a Cat With Positive Reinforcement

June 6, 2026

Tourism

Best Hidden Gems in the United States 2026 Travel Guide

April 29, 2026

Shopping

Finding the Right Fit The Best Male Running Shoes That Balance Comfort, Support, and Performance

March 20, 2026