Real Estate

What House Can I Afford A Realistic Guide to Understanding Your Home Buying Budget

April 3, 2026

Discover how to determine what house you can afford with our realistic guide. Understand your budget, hidden costs, and financial factors for a successful home purchase.

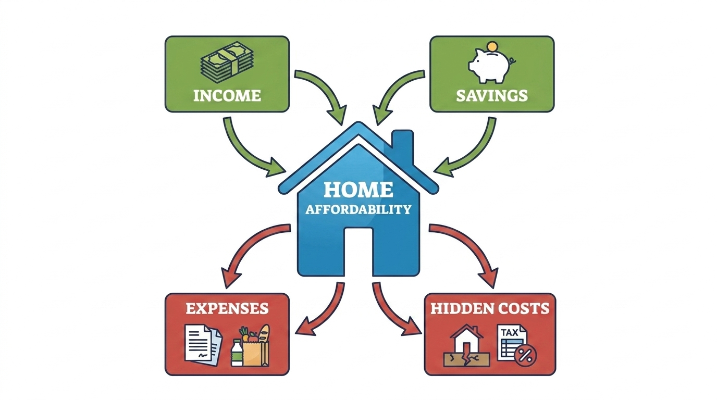

Understanding home affordability is crucial for potential homeowners as it enables informed purchasing decisions. At its core, home affordability encompasses not just how much house you can buy, but rather a broader financial picture that includes your income, savings, ongoing expenses, and often-overlooked hidden costs associated with owning a home.

Recognizing what you can realistically afford sets the foundation for a stress-free home-buying experience. It prevents the excitement of finding a dream home from being overshadowed by financial strain later on. This article aims to guide you through the intricate world of housing budgets, offering insights beyond typical affordability calculators. From evaluating your financial health to understanding the role of lenders and hidden expenses, we'll explore crucial considerations designed to empower your home-buying journey. Ultimately, our goal is to equip you with the knowledge needed to approach homeownership with confidence and clarity.

How “What House Can I Afford” Is Really Calculated

When aspiring homebuyers explore their purchasing power, understanding how lenders calculate affordability is vital. Lenders assess multiple factors, piecing together a comprehensive picture of what you can realistically afford. Here’s how they typically proceed:

Key Factors in Determining Affordability

- Income Levels: Your gross monthly income is a primary consideration. Lenders want to ensure your income is sufficient to cover the mortgage payment and other living expenses.

- Debt Levels: Outstanding debts, such as credit cards, student loans, and car loans, are factored into your financial evaluation. Higher debt levels decrease the amount you can afford for a home.

- Credit Scores: A higher credit score generally reflects responsible financial behavior and can positively influence the interest rate you’re offered, thereby impacting overall affordability.

Common Calculations Used

- Front-End Ratio: This is calculated by dividing your monthly housing costs—mortgage payments, property taxes, and insurance—by your gross monthly income. A common benchmark is that this ratio should not exceed 28%. For example, if your monthly housing costs total $2,000 and your gross income is $7,000, your front-end ratio would be approximately 28.5% (2000/7000).

- Back-End Ratio: This considers all monthly debt obligations, including housing costs, and should ideally remain below 36%. If you have $2,000 in housing costs and $1,500 in other debts, your back-end ratio would be calculated as $3,500 (2000+1500) divided by your gross income of $7,000, resulting in a back-end ratio of 50%.

Variability Among Lenders

It's essential to note that these calculations can vary significantly among different lenders and are influenced by market conditions. While one lender may adhere strictly to these ratios, another might allow for higher percentages based on factors like your credit score or the competitiveness of the local housing market.

Empowering Your Home Buying Decisions

Understanding how lenders assess home affordability through these ratios can empower buyers to make informed decisions. By considering income, debts, and credit scores, potential homeowners can better evaluate their financial readiness and set practical expectations for their home-buying journey.

Income, Debt, and the Numbers Lenders Actually Look At

When applying for a mortgage, lenders delve deeply into your financial profile to understand your overall financial health. A critical component of this assessment is income verification. Lenders typically require proof of consistent income to ensure you can handle monthly mortgage payments alongside your other financial obligations.

One pivotal metric lenders use is the debt-to-income (DTI) ratio, which compares your monthly debt payments to your gross monthly income. You can calculate your DTI by summing your monthly debts, including student loans, credit card debt, and any current mortgages. Then divide this total by your gross monthly income. For instance, if your monthly debts total $2,000 and your gross income is $6,000, your DTI ratio would be approximately 33% (2000/6000).

Lenders typically prefer a DTI ratio below 36%, indicating a manageable level of debt relative to income. High DTI ratios, particularly from student loans or excessive credit card debt, can signal risk to lenders and complicate your loan approval process.

To assess your own financial situation effectively, start by gathering your monthly income and expenses. Calculate your DTI and scrutinize where you stand. It’s wise to aim to lower your ratio by paying down debts or increasing your income, thus fostering a healthier financial profile before embarking on your home-buying journey.

Using Home Affordability Calculators the Right Way

Home affordability calculators serve as valuable tools for prospective buyers, offering quick estimates of potential budgets based on income, expenses, and current interest rates. They provide a starting point for understanding how much house you can realistically afford before diving into actual home searching. However, to maximize their usefulness, it’s crucial to input accurate figures related to your income and expenses, including monthly debts, property taxes, and insurance. This accuracy ensures the calculator reflects a realistic financial picture.

Despite their practicality, there are notable pitfalls. One common mistake is overestimating borrowing capability based solely on calculator output. For example, a buyer may input their gross income without accounting for pre-tax deductions, leading to an inflated estimate of affordability. Furthermore, calculators often fail to consider other significant financial commitments, like impending job changes, maintenance costs, or shifts in interest rates, which could impact budgeting. Therefore, while these calculators are helpful starting points, they should not replace thorough financial assessments and discussions with mortgage professionals. Always integrate these tools into a broader financial strategy to avoid miscalculations and ensure well-informed home-buying decisions.

Why Two People With the Same Income Can Afford Different Homes

Even with identical incomes, two individuals can encounter vastly different realities in homeownership. Consider Sarah, a single professional earning $80,000 annually, and the Martinez couple, whose combined income is also $80,000. Although they appear to be on equal financial ground, their home affordability varies significantly due to lifestyle choices and individual financial obligations.

Sarah lives alone and chooses to allocate a substantial portion of her earnings to experiences—traveling and dining out—which limits her ability to save. She pays $2,000 per month in rent, consuming a significant portion of her income and heavily influencing her overall financial health. Consequently, Sarah may find it challenging to save for a down payment, directly affecting her home purchasing potential.

In contrast, the Martinez couple prioritizes savings despite both working. They reside in a modest apartment with a rent of $1,200, allowing them to consistently set aside funds for their future home purchase. Their financial discipline provides them with the opportunity for a larger down payment, thereby enabling them to afford more desirable housing options, such as a suburban home, which is beyond what Sarah can realistically buy.

Ultimately, both Sarah and the Martinez family face differing student loan debts and credit card obligations that can significantly influence their purchasing power and emotional readiness to commit to a mortgage. Thus, even similar incomes can lead to differing home affordability based on personal choices and effective financial management, illustrating that it’s not solely about earnings but also about how you manage your finances.

Hidden Costs That Change Your Real Budget

When buying a home, many prospective buyers prioritize the purchase price and mortgage rates, often overlooking several hidden costs that can significantly impact their overall budget. Addressing these expenses is crucial for a true assessment of how much home you can afford. Here are some common hidden costs associated with home buying:

- Property Taxes: Local tax rates can vary notably, often increasing annually. Property taxes usually represent a percentage of the home's assessed value, implying that as property values rise, so do your taxes. This cost can result in an unexpected increase in your monthly mortgage payments.

- Homeowners' Insurance: Mortgage lenders generally require homeowners' insurance to guard against damage, but premiums can vary widely based on factors like location, coverage levels, and property condition. If you neglect to incorporate this cost into your budget, it can lead to significant financial strain.

- Maintenance and Repairs: Unlike renting, homeownership comes with ongoing maintenance obligations. Routine upkeep, appliance repairs, and emergency issues can add to your expenses. Setting aside 1-3% of your home’s value annually for these costs is prudent.

- Homeowners’ Association (HOA) Fees: Properties situated in planned communities or condominiums often incur HOA fees that cover shared amenities and maintenance. These often-overlooked expenses can dramatically impact your overall affordability, especially if they increase over time.

Considering these hidden costs is paramount when evaluating your total budget. By proactively budgeting for property taxes, insurance, maintenance, and HOA fees, you can form a clearer picture of your financial commitment, ensuring informed decisions about how much house is within your reach.

Take Control of Your Housing Budget

Navigating your housing budget can be daunting, but with a structured plan, you can confidently determine what house you can afford. Here’s how to get started:

- Consult a Mortgage Advisor: Seek guidance from a financial expert specializing in mortgages. They can provide tailored insights relevant to your financial situation, helping you comprehend various mortgage options and their implications.

- Get Pre-Approved for a Mortgage: Obtain a pre-approval letter from a lender. This document not only clarifies your budget but also enhances your position as a buyer in a competitive housing market.

- Review Your Financial Situation: Thoroughly assess your income, expenses, savings, and debts. Grasping your financial health is critical to aligning your home-buying ambitions with your long-term goals. Utilize budgeting apps or consult financial planners for assistance in this review.

- Exercise Patience: While it’s tempting to dive into homeownership, avoid hasty decisions. Take the necessary time to explore your options and make informed choices.

By following these steps, you’ll ensure that you’re making wise investments while laying the groundwork for a secure financial future. Remember, you’re not alone in this journey—countless resources, including community centers, online financial tools, and local mortgage advisors, are available to guide you along the way!

Embracing Your Journey Toward Homeownership

In closing, determining what house you can afford exceeds mere calculations of income. It necessitates a holistic view of your personal finances, taking into account savings, debt, and long-term financial aspirations. Throughout this guide, we stressed the importance of understanding hidden costs, assessing financial health accurately, and engaging effectively with lenders. By approaching the home-buying process with transparency and careful thought, you empower yourself to make decisions that align with both your current circumstances and future ambitions. With the insights shared in this article, you can navigate your housing journey with confidence, ensuring that your ideal home becomes a sustainable reality.

Just For You

Parenting

Can Babies Sleep on Their Stomach Safety Rules and Age Guidelines

May 18, 2026

Pets

The Allure of Long-Furred Cat Breeds

May 19, 2026

Tourism

Best Travel Destinations Japan A Practical Guide to Exploring Cities, Nature, and Culture

March 27, 2026

Shopping

Meaningful Choices The Ultimate Guide to Personalized Baby Gifts

April 21, 2026

Recommended For You

Parenting

Baby Weighted Sleep Sacks Safety Guidelines, Benefits, and Usage Tips

May 13, 2026

Pets

How to Toilet Train a Puppy in 7 Days

June 15, 2026

Tourism

Best Travel Destinations for Couples Thoughtful Places to Share Meaningful Moments

April 3, 2026

Shopping

Finding the Perfect Fit The Best Running Shoes for Wide Feet That Blend Comfort and Performance

March 21, 2026